Dr. Dhiraj, writing for DifferentTruths.com, explains why corporate health insurance isn’t enough and urges salaried Indians to invest in personal health insurance policies early.

AI Summary

- The Ownership Illusion: Salaried employees often mistake employer-sponsored health insurance for lifelong security, forgetting that coverage ends with employment or retirement.

- The Transition Trap: Buying personal insurance later in life leads to significantly higher premiums, rigorous underwriting, and waiting periods for pre-existing conditions.

- The Dual Strategy: The ideal approach combines corporate benefits for immediate needs with an independent personal policy to ensure lifelong, uninterrupted health ownership.

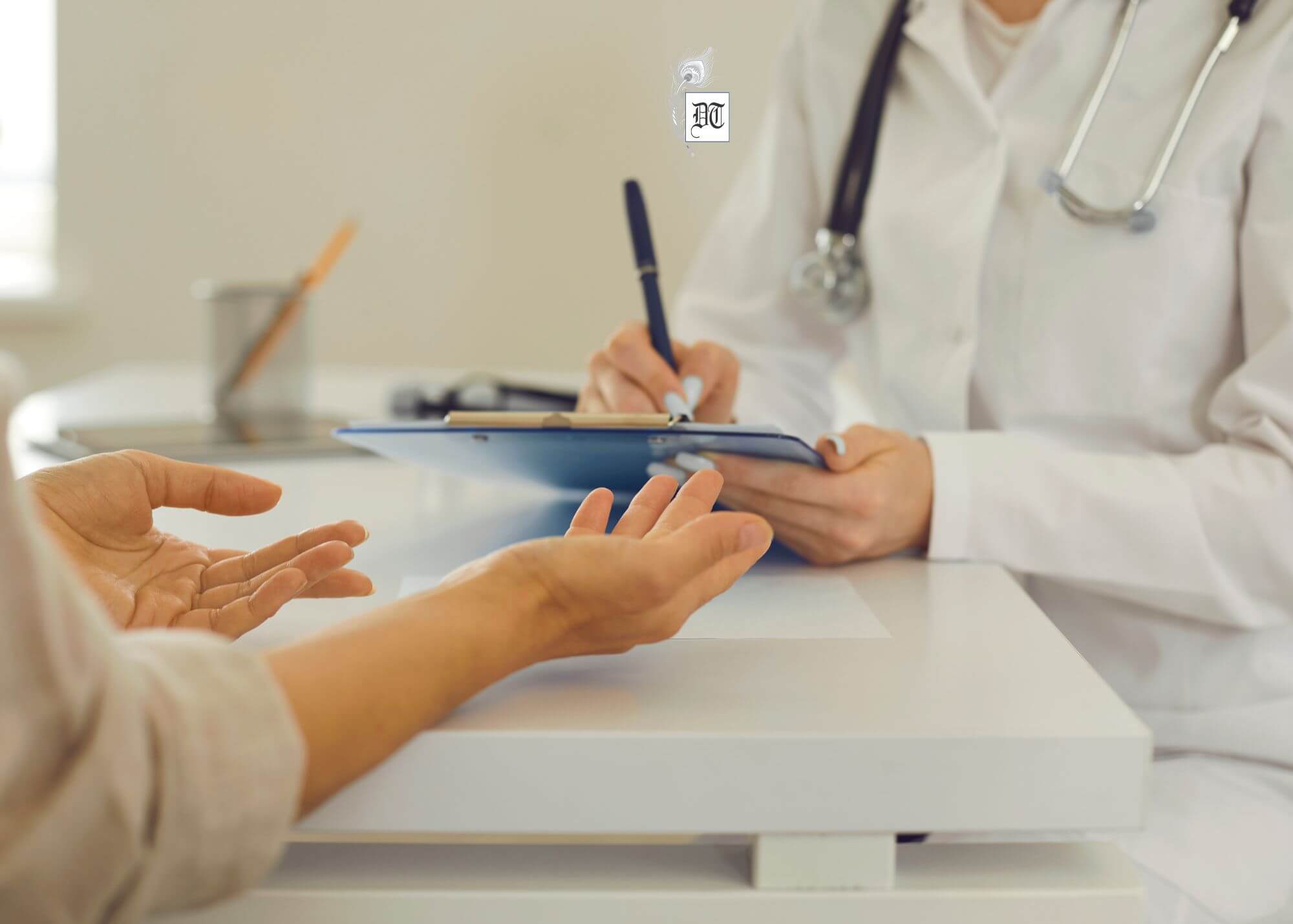

For millions of corporate salaried Indians, health insurance is something they never actively purchase. It comes automatically with the job. In addition to salary, provident fund, leave benefits, and performance incentives, employers increasingly provide health insurance coverage for employees and their families. The arrangement appears convenient and reassuring. Hospitalisation expenses are covered, cashless treatment is often available, and the employer largely handles premium payments.

As a result, many employees assume that their health insurance planning is complete. Unfortunately, that assumption can become expensive later. The problem is not that employer-provided health insurance is inadequate. In fact, many corporate policies are excellent. The problem is that employees often confuse access to insurance with ownership of insurance. Understanding this distinction is critical.

The Comfort of Corporate Health Insurance

There is no denying the advantages of employer-sponsored health insurance. Many corporate policies cover employees without extensive medical examinations. Pre-existing diseases may be covered from the very first day. Family members are often included, and premiums are either fully paid or heavily subsidised by the employer.

Consider a young professional who joins a large IT corporation at age 25. The corporation provides a family health cover of ₹5 lakhs. A few years later, maternity expenses are covered. When a child requires hospitalisation, the claim process is smooth. Over time, the employee begins to believe that health insurance is one financial concern that never needs attention. For many years, that belief appears correct.

The Hidden Limitation

A common misunderstanding is that the policy belongs to the employee, not the employer. The corporation decides the insurer, the sum insured, the policy conditions, and whether the coverage continues in future years. Employees benefit from the arrangement but do not control it.

The distinction may appear technical, but it becomes important during career transitions. A corporation can change insurers. Benefits can be revised. Coverage amounts can be modified. Most importantly, the cover usually ends when employment ends.

The Day Employment Ends

Imagine a forty-eight-year-old executive who has worked for more than twenty years and relied entirely on corporate health insurance. During these years, he develops hypertension and diabetes, but treatment remains manageable because employer insurance continues to provide coverage. Then a restructuring exercise takes place, and the job ends. For the first time, he must purchase a personal health insurance policy.

The situation is very different from what it would have been twenty years earlier. Age has increased, medical history has expanded, and premiums have risen significantly. Conditions that once seemed routine now become important during underwriting. Many people discover at this stage that obtaining health insurance is easiest when it appears unnecessary and most difficult when it appears essential.

Why Personal Health Insurance Rewards Early Planning?

Health insurance is one of the few financial products where timing matters enormously. Consider two individuals who are both fifty-five years old. One purchased a personal health insurance policy at age 35 and has maintained it continuously. The other relied entirely on employer coverage and began shopping for insurance only at fifty-five. The first individual has already completed waiting periods, accumulated continuity benefits, and established a long insurance history. The second individual is just entering the system. Although both are the same age, their insurance positions are entirely different. This is why health insurance planning should begin early, even when employer coverage already exists.

The Retirement Challenge

The importance of personal health insurance becomes even more visible at retirement. A person may spend thirty-five years enjoying comprehensive corporate medical benefits. Then retirement arrives, and the protection changes or disappears. At the very stage of life when healthcare needs become more frequent, the individual must enter the retail insurance market as a new customer. This situation is increasingly common among professionals, bankers, corporate executives, and private-sector employees.

The challenge is not merely financial. It is emotional. Medical uncertainty and financial uncertainty rarely make a comfortable combination.

The Ideal Approach: Use Both

The debate should never be framed as corporate insurance versus personal insurance. The smarter approach is to combine corporate and personal insurance. Employer coverage can serve as the first layer of protection, while personal insurance creates long-term continuity. If employment changes, personal coverage remains intact. If retirement arrives, protection continues. If health conditions develop later in life, the policy is already in place. This dual approach provides both flexibility and security.

The Final Words…

Employer health insurance is a valuable benefit, but it should never be mistaken for a complete health insurance strategy. Jobs change, employers change, and careers evolve. Health risks, however, remain throughout life. Personal health insurance provides something that employer insurance cannot—ownership. It ensures that healthcare protection remains linked to the individual rather than the organization. In financial planning, some protections should travel with you wherever life takes you. Health insurance is one of them.

In the next column, we turn to a group that often needs health insurance the most and finds it the hardest to obtain: senior citizens. We will examine why health insurance becomes more complicated after age 60 and what families can do to protect aging parents without placing excessive pressure on household finances.

Picture design by Anumita Roy

Dr Dhiraj Sharma, faculty in Management Studies at Punjabi University, Patiala, writes at the intersection of economy, finance, governance, culture, literature, and social change. His interdisciplinary work examines how individuals and institutions adapt to economic and societal shifts. Beyond academia, he pursues creative writing—fiction, non-fiction, poetry—and excels as an avid birder, nature/wildlife photographer, and painter in realistic/semi-impressionist styles. He actively supports government/NGO initiatives for bird watching, butterfly monitoring, and natural habitat conservation. He is our Associate Editor: Economy, Finance and Governance.

By

By

By

By